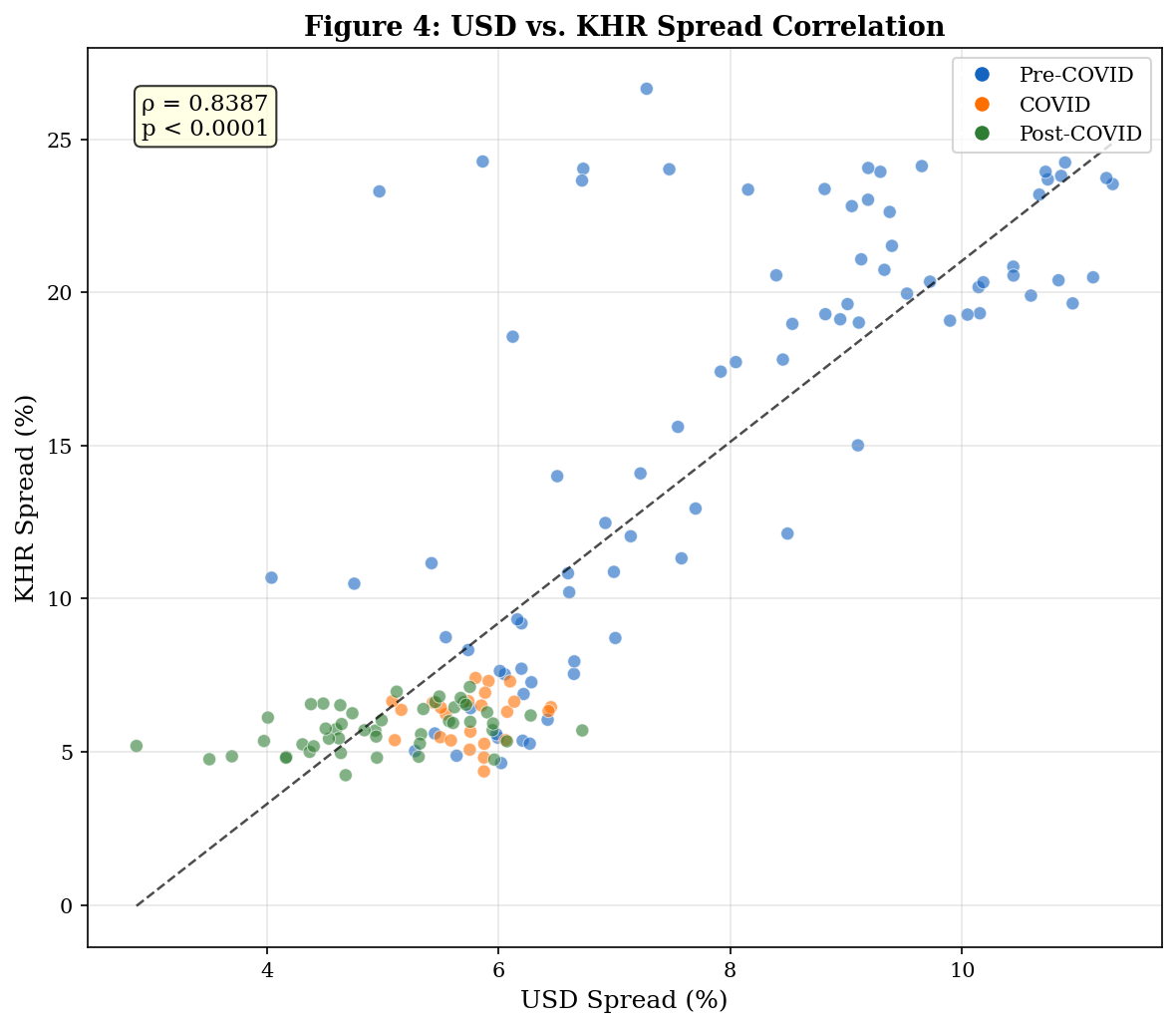

# ─── FIGURE 4: Scatter Plot ──────────────────────────────────────────────────

fig, ax = plt.subplots(figsize=(8, 7))

# Color by period

colors = []

for d in spreads.index:

if d < pd.Timestamp('2020-01-01'):

colors.append('#1565C0')

elif d < pd.Timestamp('2022-01-01'):

colors.append('#FF6F00')

else:

colors.append('#2E7D32')

scatter = ax.scatter(spreads['USD_Spread'], spreads['KHR_Spread'],

c=colors, alpha=0.6, s=40, edgecolors='white', linewidth=0.5)

# Regression line

slope, intercept, r_value, p_value, std_err = stats.linregress(

spreads['USD_Spread'], spreads['KHR_Spread'])

x_line = np.linspace(spreads['USD_Spread'].min(), spreads['USD_Spread'].max(), 100)

ax.plot(x_line, slope * x_line + intercept, 'k--', linewidth=1.2, alpha=0.7)

# Legend

from matplotlib.lines import Line2D

legend_elements = [

Line2D([0], [0], marker='o', color='w', markerfacecolor='#1565C0', markersize=8, label='Pre-COVID'),

Line2D([0], [0], marker='o', color='w', markerfacecolor='#FF6F00', markersize=8, label='COVID'),

Line2D([0], [0], marker='o', color='w', markerfacecolor='#2E7D32', markersize=8, label='Post-COVID'),

]

ax.legend(handles=legend_elements, loc='upper right')

ax.set_xlabel('USD Spread (%)')

ax.set_ylabel('KHR Spread (%)')

ax.set_title('Figure 4: USD vs. KHR Spread Correlation', fontweight='bold', fontsize=13)

ax.text(0.05, 0.95, f'ρ = {r_value:.4f}\np < 0.0001',

transform=ax.transAxes, fontsize=11, verticalalignment='top',

bbox=dict(boxstyle='round', facecolor='lightyellow', alpha=0.8))

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.savefig('../figures/fig4_correlation.png', dpi=300, bbox_inches='tight')

plt.show()

print('Saved: fig4_correlation.png')