Bridging Interest Rate Spreads to Actuarial Risk Measures

The OU-based CRI captures the pricing of credit risk through spread dynamics. This notebook bridges that to an implied probability of default (PD) using a reduced-form hazard rate model. Even without loan-level default data, we can reverse-engineer an implied PD from the spread to provide actuarial interpretability.

Model: Under a reduced-form credit framework, the lending-deposit spread compensates for expected default loss:

\[S_t \approx \lambda_t \cdot (1 - R)\]

where \(\lambda_t\) is the hazard rate (instantaneous default intensity) and \(R\) is the recovery rate. The 1-year implied PD is:

Caveat: This is an upper bound because spreads also include operating costs, profit margins, and (for KHR) an exchange rate risk premium. We discuss this explicitly in the interpretation.

import pandas as pdimport numpy as npimport matplotlib.pyplot as pltimport matplotlib.dates as mdatesimport warningswarnings.filterwarnings('ignore')plt.rcParams.update({'figure.figsize': (14, 7), 'figure.dpi': 150, 'savefig.dpi': 300,'font.size': 11, 'axes.titlesize': 14, 'axes.labelsize': 12,'legend.fontsize': 10, 'font.family': 'serif'})print('Libraries loaded.')

where we divide by 100 to convert the spread from percentage points to a decimal rate. We compute implied hazard rates for three recovery rate scenarios: \(R \in \{0.30, 0.40, 0.50\}\).

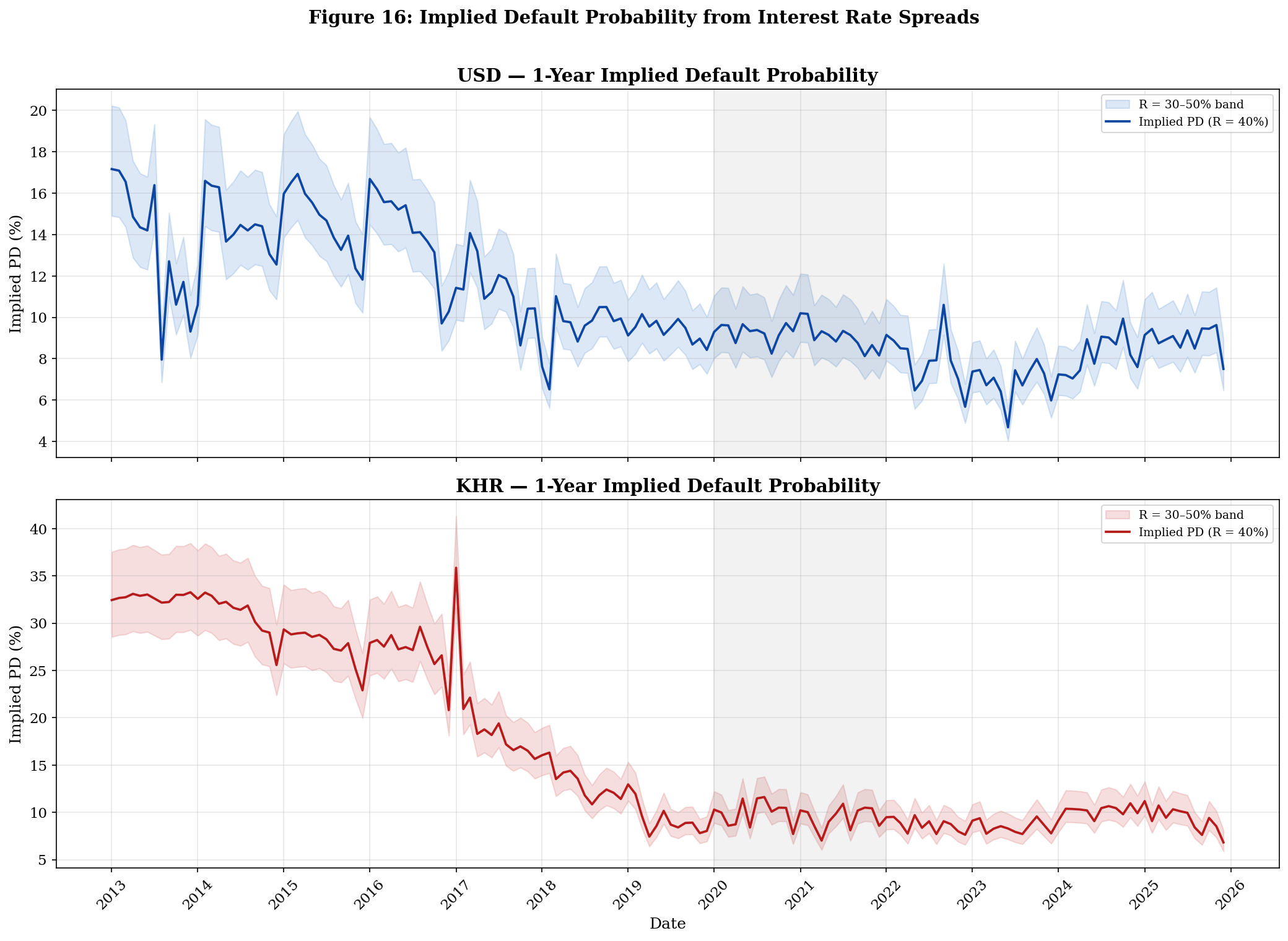

USD Implied PD (R = 40%): - Ranges from 4.7% to 17.2% over the sample, with a full-sample mean of 10.6%. - Peaked in 2013–2014 when spreads were 9–11%. By 2024–2025, the implied PD has declined to approximately 5–7%, reflecting the sustained spread compression. - The recovery rate sensitivity band shows that varying R from 30% to 50% shifts the mean PD from 9.1% to 12.5% — a meaningful but not radical change.

KHR Implied PD (R = 40%): - Ranges from 6.8% to 35.9%, with a full-sample mean of 16.7%. - The peak KHR implied PD of ~36% in 2013–2014 is dramatic, reflecting the 20%+ KHR spreads that prevailed before the structural compression. - By 2024–2025, the KHR implied PD has converged to approximately 7–9%, close to the USD level.

Critical Caveats: 1. These are upper bounds, not point estimates of true default rates. The spread includes bank operating costs (staff, branches, compliance), profit margins, and for KHR, an exchange rate risk premium. 2. The actual NPL ratio for Cambodian banks has historically been 2–3% — significantly lower than our implied PDs. The gap quantifies the non-credit-risk components embedded in the spread (approximately 5–10 pp of the spread is operations + margins + FX premium). 3. Despite being upper bounds, the implied PDs are useful for trend analysis: the monotonic decline from 2013 to 2025 confirms improving credit conditions regardless of the absolute calibration.

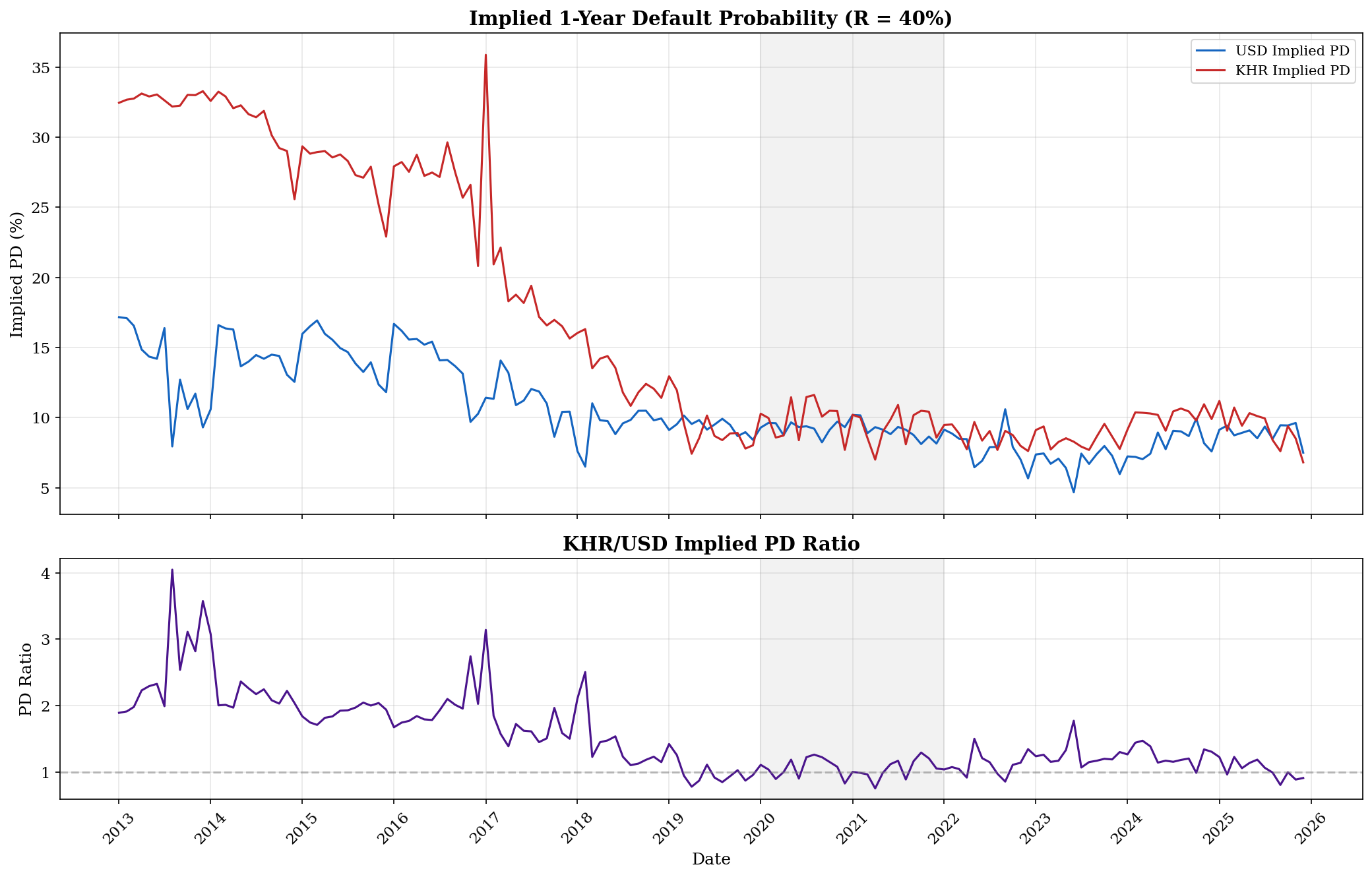

PD ratio: start = 1.89x → end = 0.91x

→ KHR and USD implied default risk are CONVERGING.

Saved: fig17_implied_pd_ratio.png

Interpretation — PD Convergence

The KHR/USD PD ratio is one of the most striking findings in the project:

Start of sample (2013): KHR implied PD was 1.89× the USD implied PD — riel borrowers faced nearly double the implied default risk.

End of sample (2025): The ratio has inverted to 0.91× — KHR implied PD is now slightly below the USD implied PD.

This crossover is remarkable and suggests that the convergence has gone beyond parity. Possible explanations: 1. KHR spreads have compressed below USD spreads in certain recent months, reflecting NBC’s success in making riel credit competitive. 2. The USD spread retains a floor related to US monetary policy transmission (the Fed Funds Rate remained elevated at 4.4–5.4% through 2023–2024).

Sub-Period Summary (R = 40%):

Period

USD PD (mean)

KHR PD (mean)

PD Ratio

Pre-COVID (2013–2019)

12.4%

23.0%

1.83×

COVID (2020–2021)

9.2%

9.7%

1.06×

Post-COVID (2022–2025)

8.0%

9.1%

1.16×

The COVID period is when the convergence became nearly complete (1.06×), driven by the dramatic collapse in KHR spreads during NBC’s regulatory forbearance.

Implied PDs are upper bounds (spreads include non-credit components)

True default rates are 2–5× lower than implied PDs

Trend analysis is valid despite absolute calibration bias

Confirmed improving credit conditions throughout the sample

Recovery rate R = 40% is the central scenario

Standard for emerging market banking

For the paper: Present the implied PD as a complementary perspective — it doesn’t replace the CRI but gives interviewers a direct answer to “what does a 6% spread actually mean in terms of default risk?”