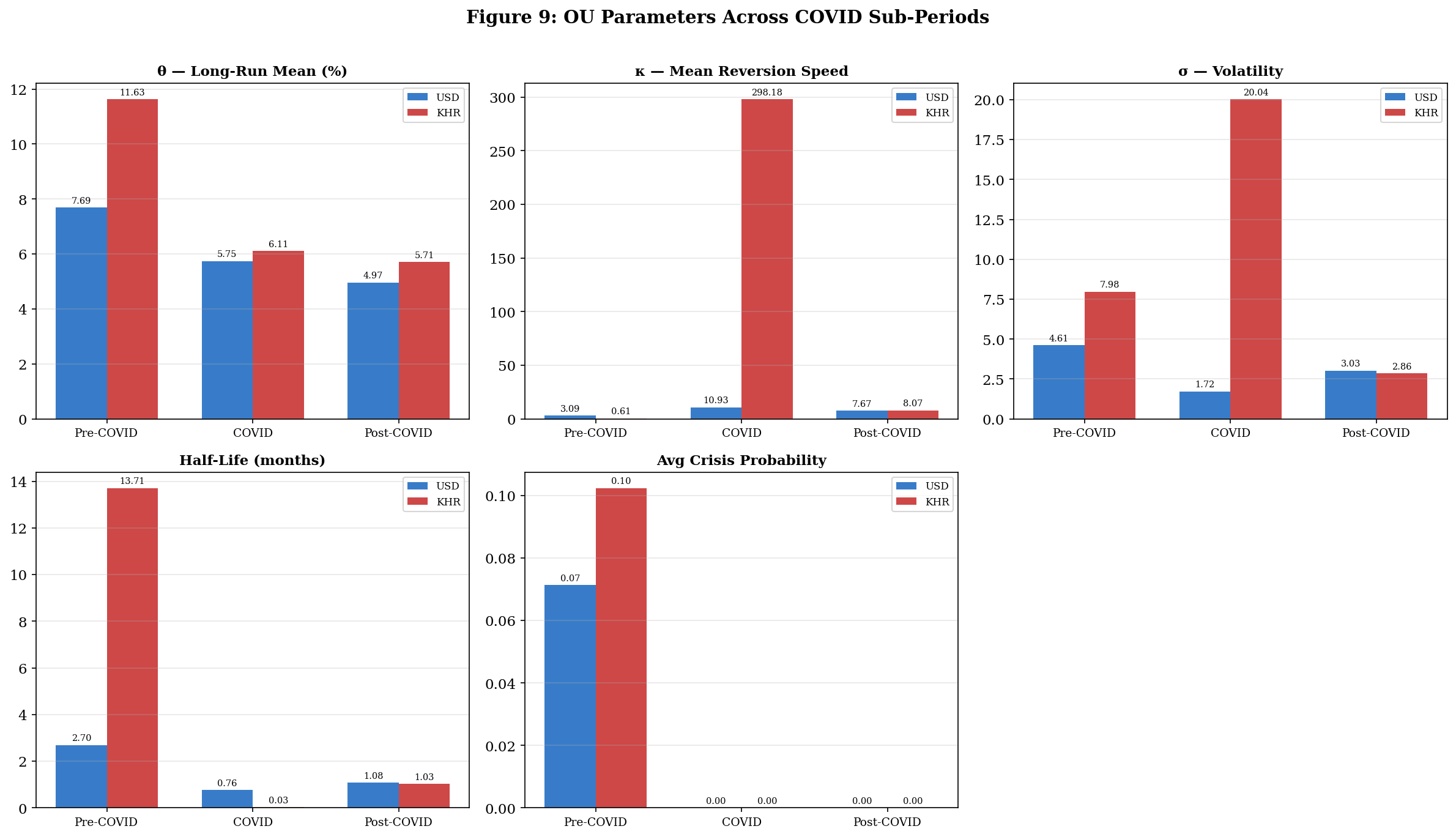

# ─── FIGURE 9: Parameter Comparison ──────────────────────────────────────────

fig, axes = plt.subplots(2, 3, figsize=(16, 9))

period_names = [r['Period'] for r in results]

x = np.arange(len(period_names))

width = 0.35

params_to_plot = [

('θ — Long-Run Mean (%)', 'θ_USD', 'θ_KHR'),

('κ — Mean Reversion Speed', 'κ_USD', 'κ_KHR'),

('σ — Volatility', 'σ_USD', 'σ_KHR'),

('Half-Life (months)', 'HL_USD', 'HL_KHR'),

('Avg Crisis Probability', 'P_USD', 'P_KHR'),

]

for idx, (title, col_usd, col_khr) in enumerate(params_to_plot):

ax = axes.flat[idx]

vals_usd = [r[col_usd] for r in results]

vals_khr = [r[col_khr] for r in results]

bars1 = ax.bar(x - width/2, vals_usd, width, label='USD', color='#1565C0', alpha=0.85)

bars2 = ax.bar(x + width/2, vals_khr, width, label='KHR', color='#C62828', alpha=0.85)

ax.set_title(title, fontweight='bold', fontsize=11)

ax.set_xticks(x)

ax.set_xticklabels(period_names, fontsize=9)

ax.legend(fontsize=8)

ax.grid(True, alpha=0.3, axis='y')

for bars in [bars1, bars2]:

for bar in bars:

h = bar.get_height()

ax.annotate(f'{h:.2f}', xy=(bar.get_x()+bar.get_width()/2, h),

xytext=(0, 2), textcoords='offset points', ha='center', va='bottom', fontsize=7)

axes.flat[5].set_visible(False)

fig.suptitle('Figure 9: OU Parameters Across COVID Sub-Periods', fontweight='bold', fontsize=14, y=1.01)

plt.tight_layout()

plt.savefig('../figures/fig9_covid_comparison.png', dpi=300, bbox_inches='tight')

plt.show()

print('Saved: fig9_covid_comparison.png')