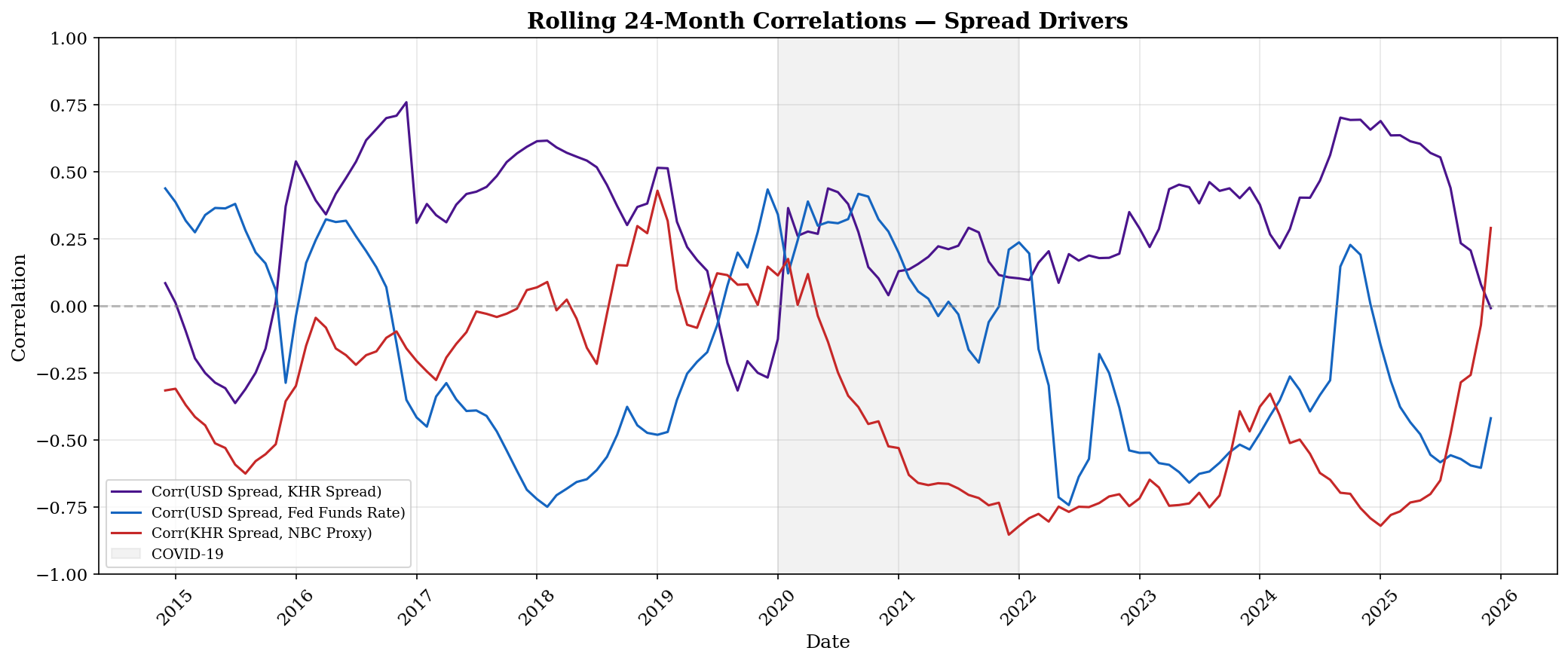

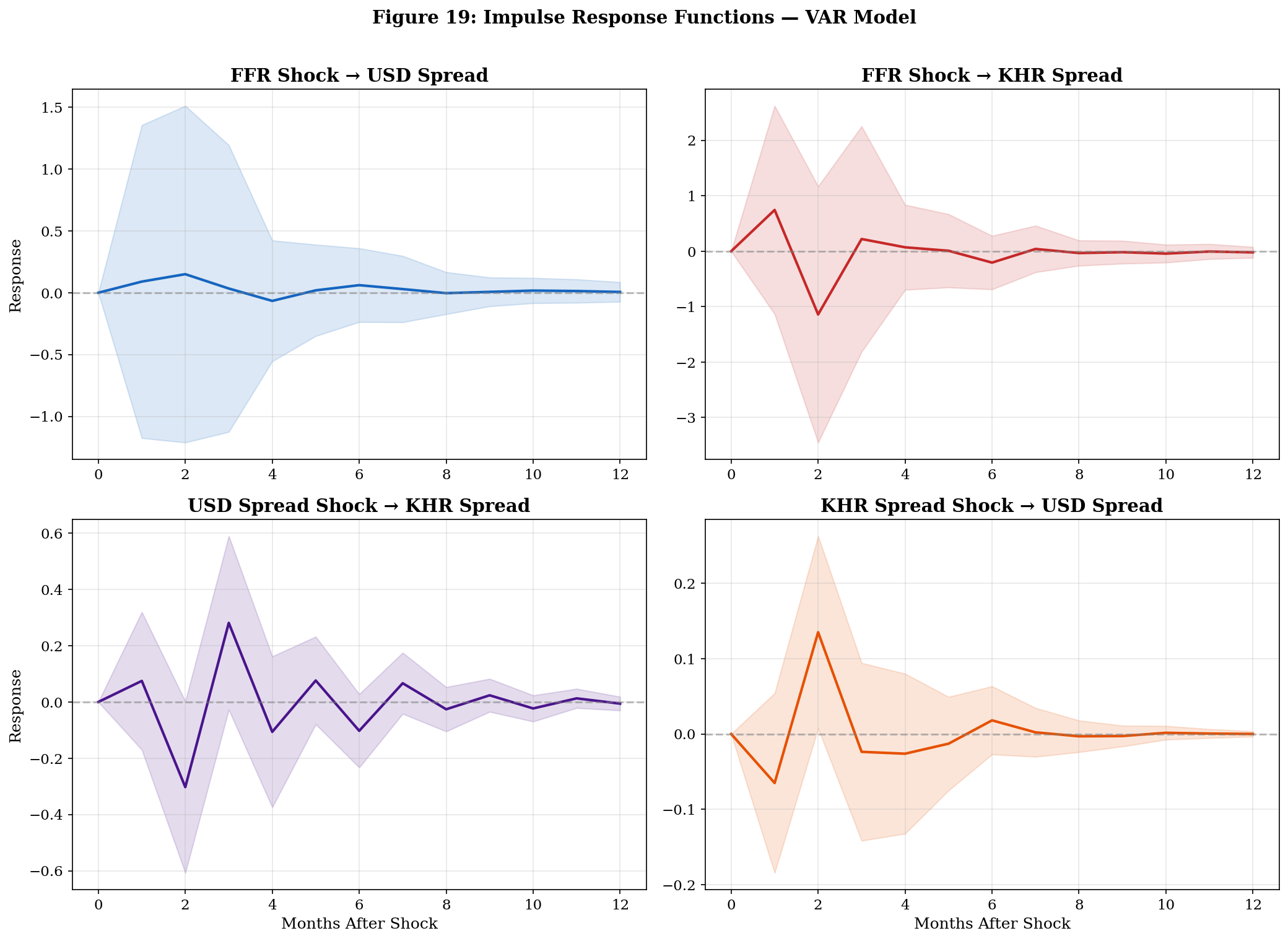

# ─── Impulse Response Functions ──────────────────────────────────────────────

irf = var_result.irf(periods=12)

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

# Identify column indices

col_names = list(data_diff.columns)

usd_idx = col_names.index('S_USD')

khr_idx = col_names.index('S_KHR')

ffr_idx = col_names.index('FFR')

# FFR shock → USD Spread

ax = axes[0, 0]

ax.plot(irf.irfs[:, usd_idx, ffr_idx], color='#1565C0', linewidth=2)

ax.fill_between(range(13), irf.irfs[:, usd_idx, ffr_idx] - 1.96*irf.stderr()[:, usd_idx, ffr_idx],

irf.irfs[:, usd_idx, ffr_idx] + 1.96*irf.stderr()[:, usd_idx, ffr_idx],

alpha=0.15, color='#1565C0')

ax.axhline(y=0, color='grey', linestyle='--', alpha=0.5)

ax.set_title('FFR Shock → USD Spread', fontweight='bold')

ax.set_ylabel('Response')

ax.grid(True, alpha=0.3)

# FFR shock → KHR Spread

ax = axes[0, 1]

ax.plot(irf.irfs[:, khr_idx, ffr_idx], color='#C62828', linewidth=2)

ax.fill_between(range(13), irf.irfs[:, khr_idx, ffr_idx] - 1.96*irf.stderr()[:, khr_idx, ffr_idx],

irf.irfs[:, khr_idx, ffr_idx] + 1.96*irf.stderr()[:, khr_idx, ffr_idx],

alpha=0.15, color='#C62828')

ax.axhline(y=0, color='grey', linestyle='--', alpha=0.5)

ax.set_title('FFR Shock → KHR Spread', fontweight='bold')

ax.grid(True, alpha=0.3)

# USD Spread shock → KHR Spread (cross-currency spillover)

ax = axes[1, 0]

ax.plot(irf.irfs[:, khr_idx, usd_idx], color='#4A148C', linewidth=2)

ax.fill_between(range(13), irf.irfs[:, khr_idx, usd_idx] - 1.96*irf.stderr()[:, khr_idx, usd_idx],

irf.irfs[:, khr_idx, usd_idx] + 1.96*irf.stderr()[:, khr_idx, usd_idx],

alpha=0.15, color='#4A148C')

ax.axhline(y=0, color='grey', linestyle='--', alpha=0.5)

ax.set_title('USD Spread Shock → KHR Spread', fontweight='bold')

ax.set_ylabel('Response')

ax.set_xlabel('Months After Shock')

ax.grid(True, alpha=0.3)

# KHR Spread shock → USD Spread (reverse spillover)

ax = axes[1, 1]

ax.plot(irf.irfs[:, usd_idx, khr_idx], color='#E65100', linewidth=2)

ax.fill_between(range(13), irf.irfs[:, usd_idx, khr_idx] - 1.96*irf.stderr()[:, usd_idx, khr_idx],

irf.irfs[:, usd_idx, khr_idx] + 1.96*irf.stderr()[:, usd_idx, khr_idx],

alpha=0.15, color='#E65100')

ax.axhline(y=0, color='grey', linestyle='--', alpha=0.5)

ax.set_title('KHR Spread Shock → USD Spread', fontweight='bold')

ax.set_xlabel('Months After Shock')

ax.grid(True, alpha=0.3)

fig.suptitle('Figure 19: Impulse Response Functions — VAR Model', fontweight='bold', fontsize=14, y=1.01)

plt.tight_layout()

plt.savefig('../figures/fig19_irf.png', dpi=300, bbox_inches='tight')

plt.show()

print('Saved: fig19_irf.png')